Takeaways

- The study looked at whether a mortgage borrower of a different race pays more or less than a similarly qualified borrower of the same race when using the same broker.

- The results suggested that the race of the borrower and the broker did influence the amount of mortgage fees paid.

- The authors didn’t find definitive proof of why the price disparity is happening.

With mortgage rates at an all-time low during the pandemic, 2020 is a good year to buy a home. Remote work and virtual school opened up avenues for new types of living arrangements and made once-distant geographies seem more appealing. Early data shows people are leaving major metros — such as New York City and San Francisco — for suburbs and states offering more space for a lower price, with the bonus of a neighborhood pool and a tennis court.

This quality-of-life upgrade has major implications for the future of cities and towns, possibly deepening the divide between the “haves” who can afford to move and the “have-nots” who can’t. The hasty shift also raises questions about the types of loans borrowers are signing and the fees they’re paying to secure a new home as quickly as possible.

For minority borrowers, questions about fee transparency could be particularly fraught with uncertainty. In recent years, studies unveiled the barriers to fair housing that exist for many borrowers across the country, and several major banks settled lawsuits alleging Black and Latinx borrowers were steered toward riskier and more expensive mortgages.

Now new research from the University of Georgia’s Terry College of Business and Pennsylvania State University’s Smeal College of Business could shed additional light into how some of those pricing disparities occur in mortgage contracts.

The paper, forthcoming in the Review of Financial Studies, focuses on the race of both the borrower and the broker of a mortgage loan. Notably, the research team found minority borrowers “pay a premium relative to white borrowers when they obtain loans through white brokers.” But there is some evidence that “white borrowers pay higher fees when obtaining a loan through a minority broker.” The researchers investigated a dataset from a major U.S. lender and analyzed trends among individual brokers, which revealed several unique findings.

“People always talk about your house being your largest financial asset, and the evidence is here that the race of the broker seems to matter and lead to different treatment,” says James Conklin, one of the study authors and an associate professor of real estate at the Terry College.

The research team looked at whether a borrower of a different race pays more or less than a similarly qualified borrower of the same race when using the same broker by including mortgage broker fixed effects in their analysis.

Controlling for the individual broker reduces, but does not eliminate mortgage pricing differences. In fact, the remaining unexplained pricing gaps fall within the range of pricing differences that triggered legal action against lenders in the past for discrimination.

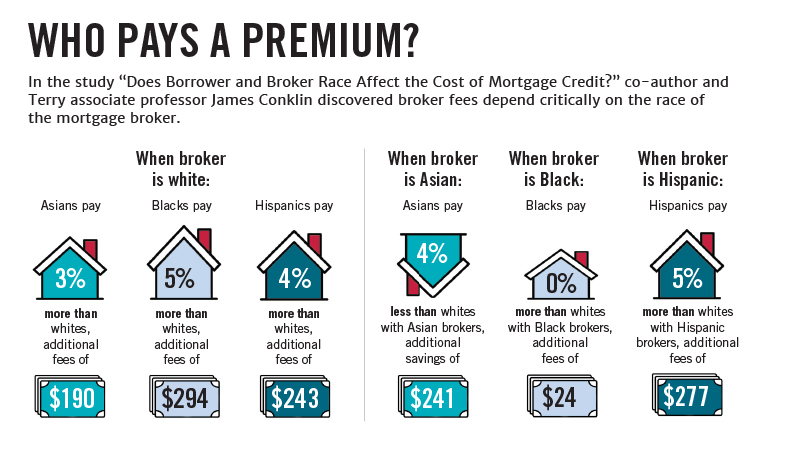

The amount of pricing disparities depends on both the borrower and broker’s race or ethnicity. For example, when the broker is white, Black borrowers pay 5% more, on average, than white borrowers, adding up to an additional $294 in mortgage fees. Hispanic borrowers pay about 4% more than white borrowers, with about $243 more in fees, and Asian borrowers pay 3% more than white borrowers, about $190 more.

On the other hand, Black brokers don’t appear to charge different fees to white and Black borrowers, and Hispanic brokers charge Hispanic borrowers more. For Asian brokers, there is evidence Asian borrowers receive more favorable treatment relative to white borrowers.

Brent Ambrose, director of the Penn State Institute for Real Estate Studies, and Luis Lopez, assistant professor of real estate at the University of Illinois at Chicago, collaborated with Conklin on the research.

Although the team’s data can’t provide definitive proof of why this is happening, the results do suggest that race of the borrower and the broker influence mortgage fees paid. The team ruled out statistical discrimination, which would require fee differences to be independent of the broker’s race, as well as other causes such as a borrower’s credit risk.

“After controlling for the variables and seeing the smaller difference in fees, this tells us that minorities tend to end up with more expensive brokers,” Conklin says. “The premium they end up paying is small but important, and somehow they’re being sought out or finding those types of more expensive brokers.”

Settling a lawsuit in Philadelphia

Ultimately, the findings are in line with the major lawsuits filed in recent years, Conklin says, and new research will continue to play a role in regulations and policies that try to address disparities in the mortgage industry. For one, Conklin and the team plan to study additional factors related to race and ethnicity — as well as the gender of borrowers and brokers.

One such lawsuit was resolved last year. Wells Fargo & Co. agreed to pay $10 million to the City of Philadelphia in December 2019 to settle a federal lawsuit filed in 2017 claiming the bank violated the Fair Housing Act and discriminated against minority borrowers. The company disputed the claims but agreed to a settlement that would fund several of the city’s existing fair housing programs in 2020.

“During these difficult times, it is critical that families have housing stability and begin to accumulate wealth,” said Marcel Pratt, the city solicitor for Philadelphia.

The city’s complaint focused on a regression analysis of data, which controlled for race and objective risk factors such as a borrower’s credit history, loan-to-value ratio, and loan-to-income ratio. Between 2004 to 2014, the city found, Black borrowers with a 660 credit score or higher were 2.6 times more likely to receive a more expensive or risky loan than a white borrower with similar credit factors. Latinx borrowers were 2.1 times more likely to receive a more expensive or risky loan.

“We needed the data and research in order to show the stark effects of these discriminatory practices on communities of color,” Pratt said. “It is already undeniable that communities of color face barriers to homeownership, but the data and research on discrimination in housing made our case more persuasive.

What changes may come

In the wake of the 2007-2008 financial crisis, lawmakers and regulators focused on curbing abuses in mortgage lending and broker business practices. The Mortgage Reform and Anti-Predatory Lending Act, which was passed in 2010 as part of the Dodd-Frank Act, suggested restricting broker compensation that might motivate them to push borrowers toward riskier and more expensive loans. In particular, regulators considered banning dual compensation, which allows the broker to earn dollars on both sides — through mortgage fees from the borrower and rebates from the lender. At this time, dual compensation isn’t prohibited, but the Consumer Financial Protection Bureau has expressed interest in investigating it further.

As part of their analysis, Conklin and colleagues designed a test to understand the consequences of restricting dual compensation. Overall, minority borrowers still paid higher fees, despite the type of loan and broker compensation, so a regulation banning that practice is unlikely to eliminate racial price disparities.

However, other regulations could harm minority borrowers, the research team found. If broker fees are capped, for instance, about 25% of Black and Hispanic borrowers who worked with white brokers could have been credit rationed, as compared with 16% of white borrowers and 6% of Asian borrowers. Although fee caps are intended to make loans affordable and reduce a broker’s influence on pricing, the caps could also prompt brokers to withdraw from borrower applications that require extra effort or services, they found.

“For some borrowers, it’s more costly to originate a loan, and they may require more hand-holding and paperwork,” Conklin said. “Under a fee cap, a broker could lose money originating a loan and decide not to do it. The punchline is that fee caps may hit minority borrowers the hardest.”

Even still, positive shifts are happening this year. With the $10 million settlement from Wells Fargo, Philadelphia has infused $8.5 million into grants for down payment and closing cost assistance for low- and moderate-income residents who purchased homes in the city. Another $500,000 funded the city’s revitalization program that refurbishes vacant land by cleaning and planting vegetation in abandoned residential lots, and that work is ongoing this year.

Another $1 million will be divided among two nonprofit organizations that try to prevent foreclosures in the city. In the past, the program has helped low-income and minority residents to stay in their homes, and it streamlined the legal process in the court system. Due to pandemic-related court closures, the program’s activities have been stalled, but the city intends to start up assistance again soon. In the meantime, homeowners can receive housing counseling services.

The settlement has helped on a personal level as well. Between July 2019 and July 2020, nearly 2,000 households received funds for down payments and closing costs. Though there’s still more work to do in closing the gap for minority homeowners in Philadelphia, it’s a start.

“These programs help first-time homeowners obtain their goals,” Pratt said. “Homeownership is one of the most effective ways that families accumulate wealth in America.”